Ideal Tips About What Is Arima Vs Garch Model Draw A Line Chart

Arimagarch Model Estimation Results. Download Scientific Diagram Regression Graph In Excel How To Change The Vertical Axis Values

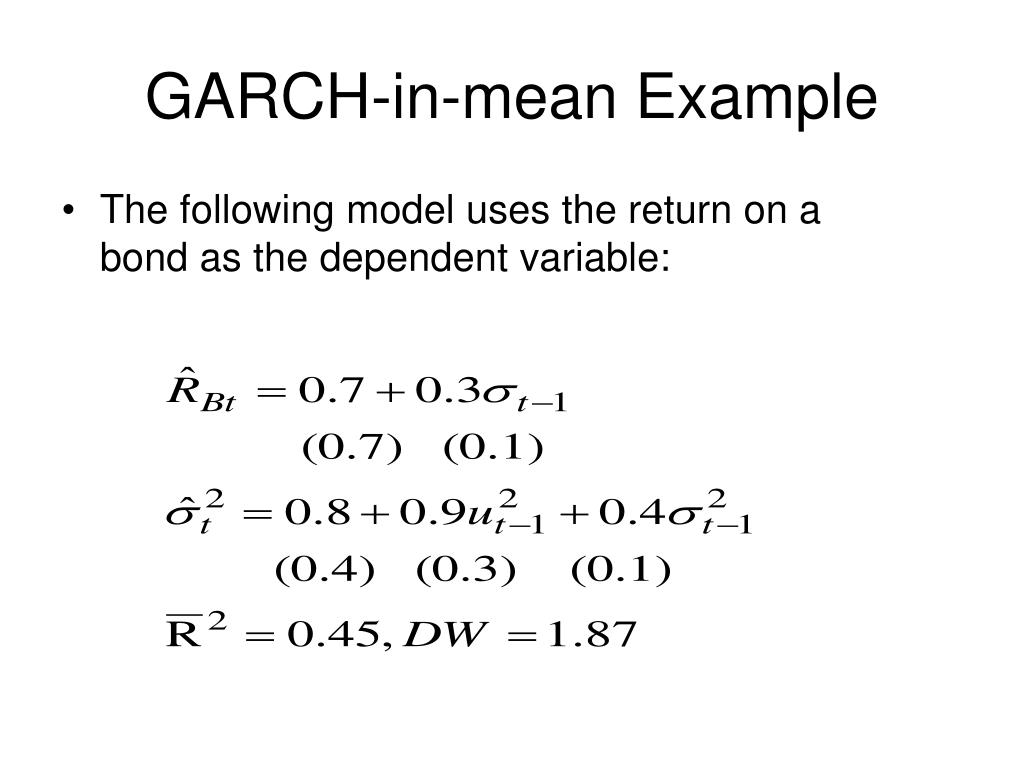

Garch Model Example 1 Turjn Excel How To Change Graph Scale Add Line In Bar

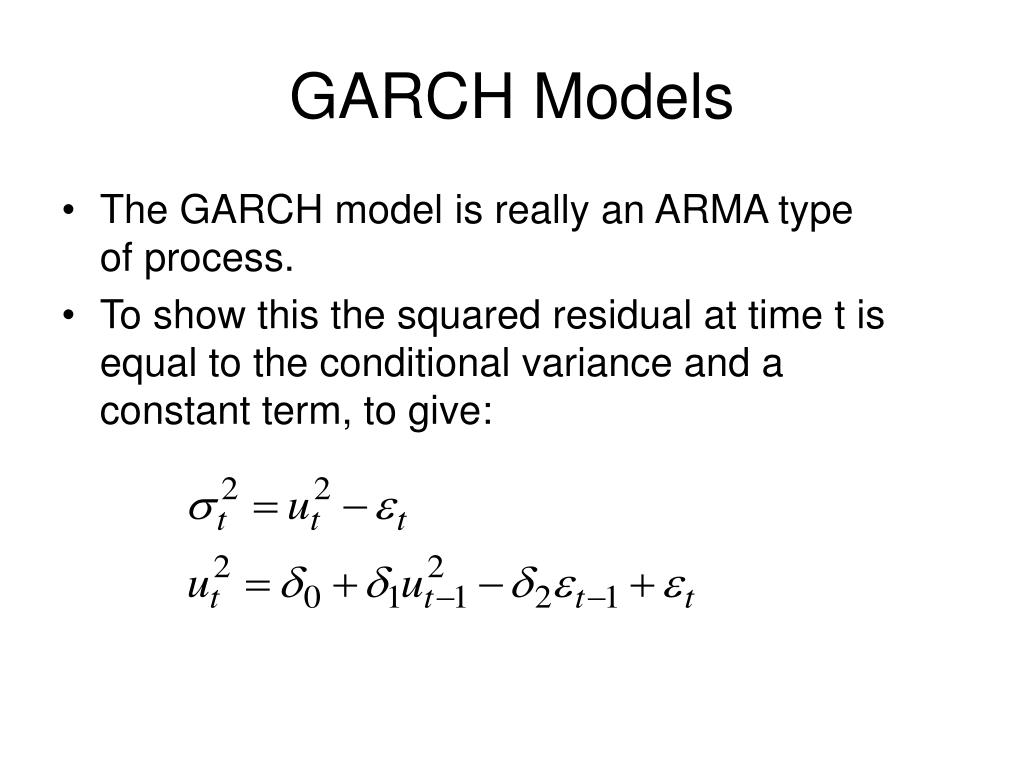

Ppt Garch Models And Asymmetric Powerpoint Presentation Change Scale Of Graph In Excel Types Trends Line Graphs

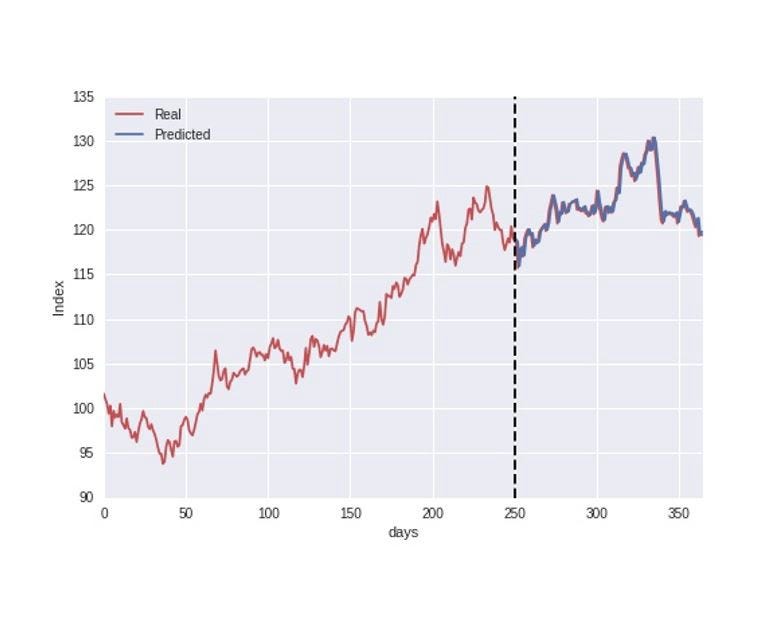

Arimagarch Forecasting With Python By Thomas Dierckx Analytics Combo Chart Excel 2010 Dual Axis Map In Tableau

Introduction To Volatility Models With Matlab (arch, Garch, Gjrgarch Ggplot2 Line Graph Multiple Lines Draw A Curve In Excel

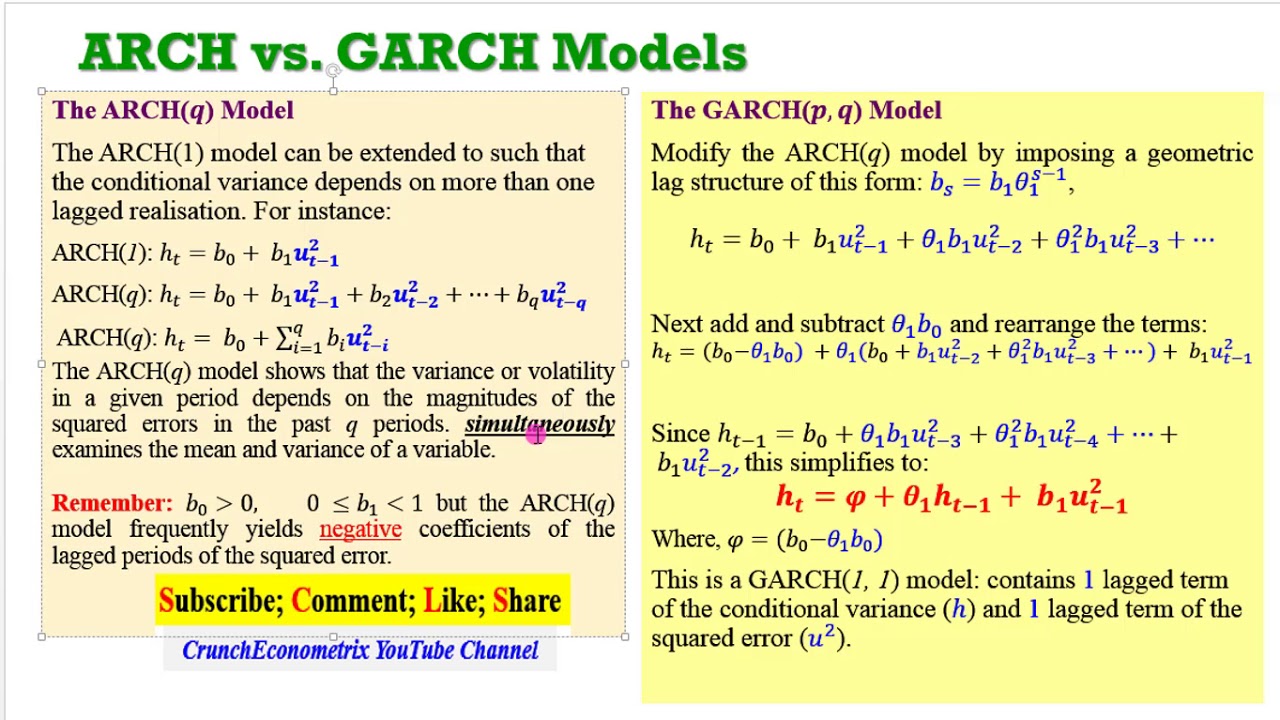

Arch Vs Garch (the Background) Clustering Volatility Bezier Curve Excel Chart Js Multiple Lines

If the series of conditional variances were observable, you could apply arima on it.

What is arima vs garch model. Arima is a fundamental time series model. However, conditional variances are not observable, so you. I am currently working on arma+garch model using r.

This post discusses the autoregressive integrated moving average model (arima) and the autoregressive conditional heteroskedasticity model (garch). For each day, n, the previous k days of the differenced logarithmic returns of a stock market index are used as a window for fitting an optimal arima and garch model. I am looking out for example which explain step by step explanation for fitting this model in r.

Pick the garch model orders according to the arima model with the lowest aic. Garch has also proven efficient for financial time series, since it can extract more complex patterns from a time series compared to arma and arima models. This model contains an lstm input layer which.

Arma(1, 0) ( 1, 0) with the ar coefficient >1), not necessarily an arima. Additionally it provides a comparison of two models: Forecast using a chosen model which is arima (auto regressive integral moving average) model in our case.

Arch models (garch is just a more general. This article serves as an overview of a powerful yet simple model known as arima. Describing the behavior of a time series is challenging for a quantitative researcher because there is a phenomenon of volatility clustering and.

Auto regressive integrated moving average (arima) models and a similar concept known as auto regressive conditional heteroskedasticity (arch) models will. Then forecast its volatility(residuals) using a. When it comes to financial time series (ts) modelling, autoregressive models (models that makes use of previous values to forecast the.

Iterate through combinations of arima(p, d, q) models to best fit our time series. In this paper, we introduce a hybrid approach using the arima and lstm models collectively. Models we will implement are as follow: autoregressive integrated moving average model, arima.

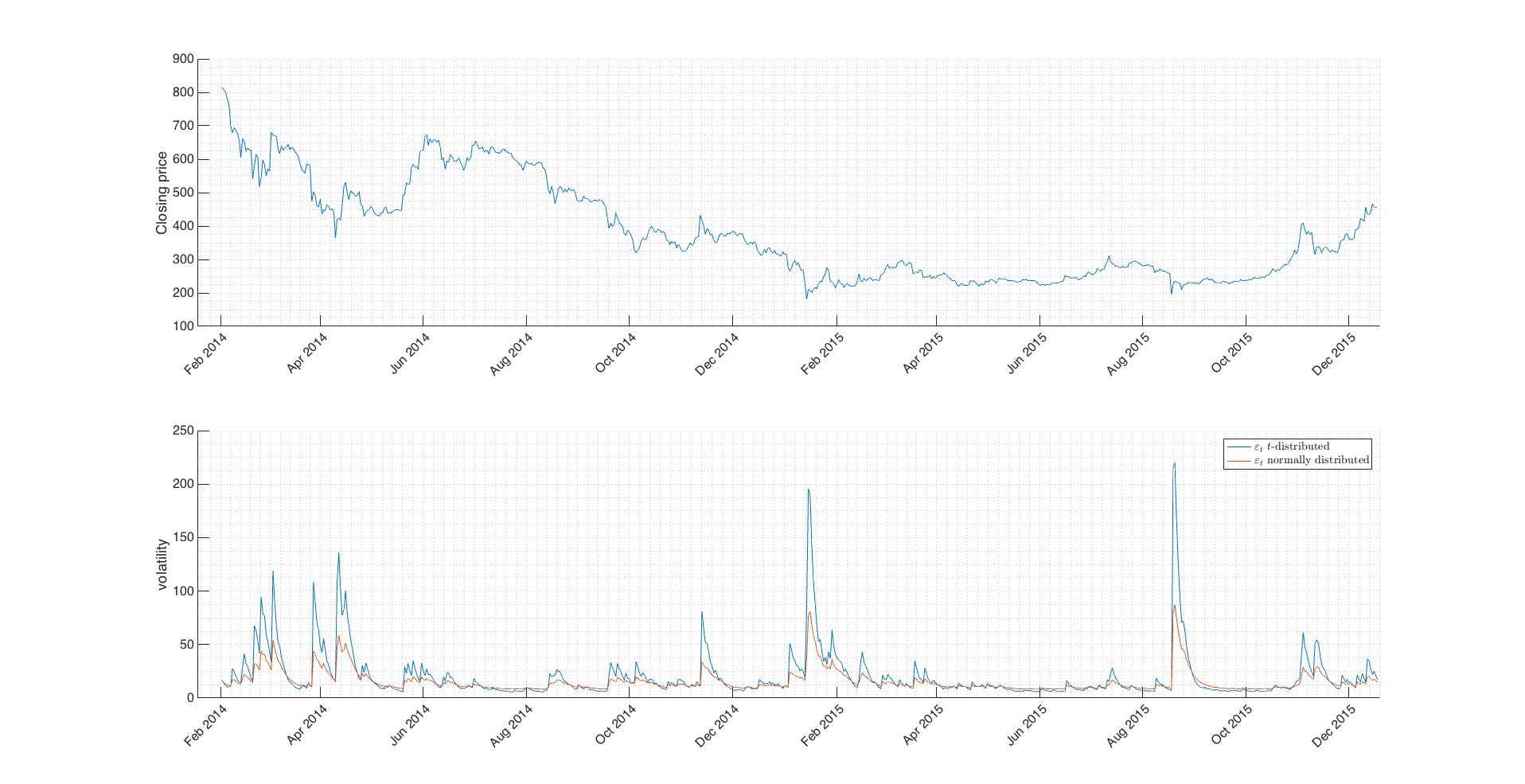

A nonstationary arma can be just that, a nonstationary arma (e.g. Below you can see the volatility forecasts after fitting an arch (11) model on the s&p500 price returns.

Ppt Garch Models And Asymmetric Powerpoint Presentation How To Label Data Points In Excel Scatter Plot Trendline Tool

Modelli Arima+garch How To Add Regression Line Scatter Plot In Excel Semi Log Graph Paper

Ppt Garch Models And Asymmetric Powerpoint Presentation Ggplot Legend Two Lines Time Series Chart In Excel

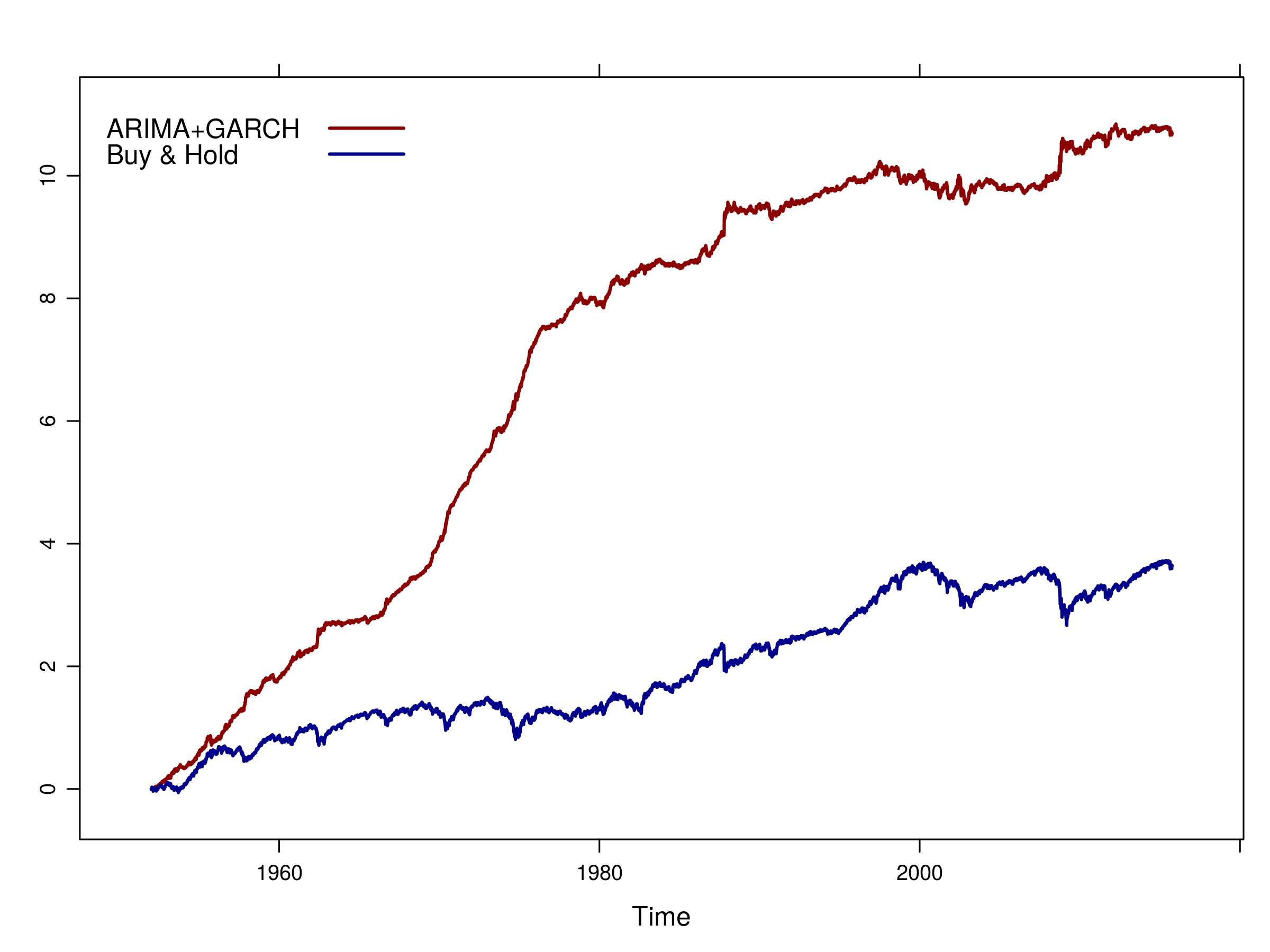

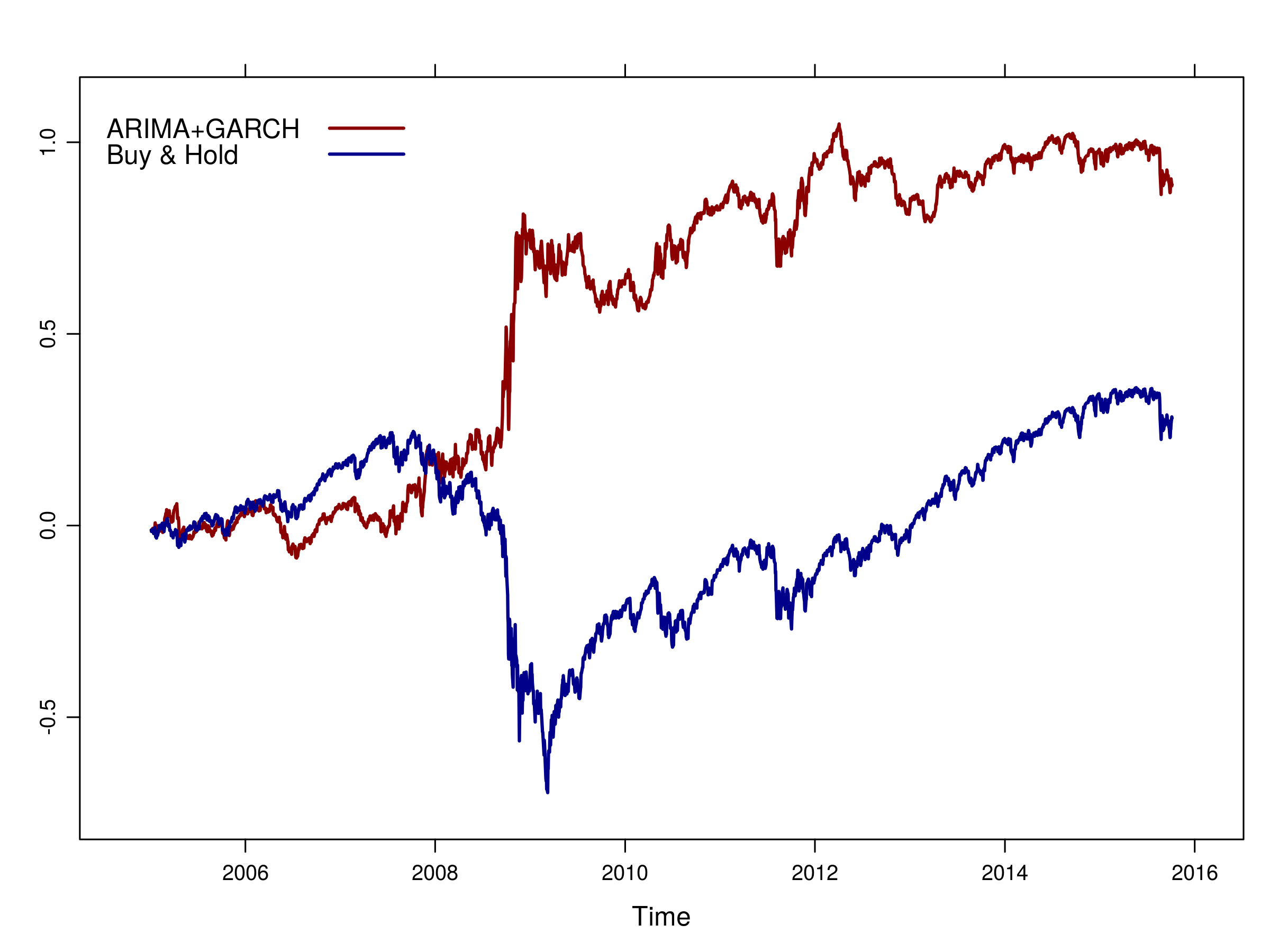

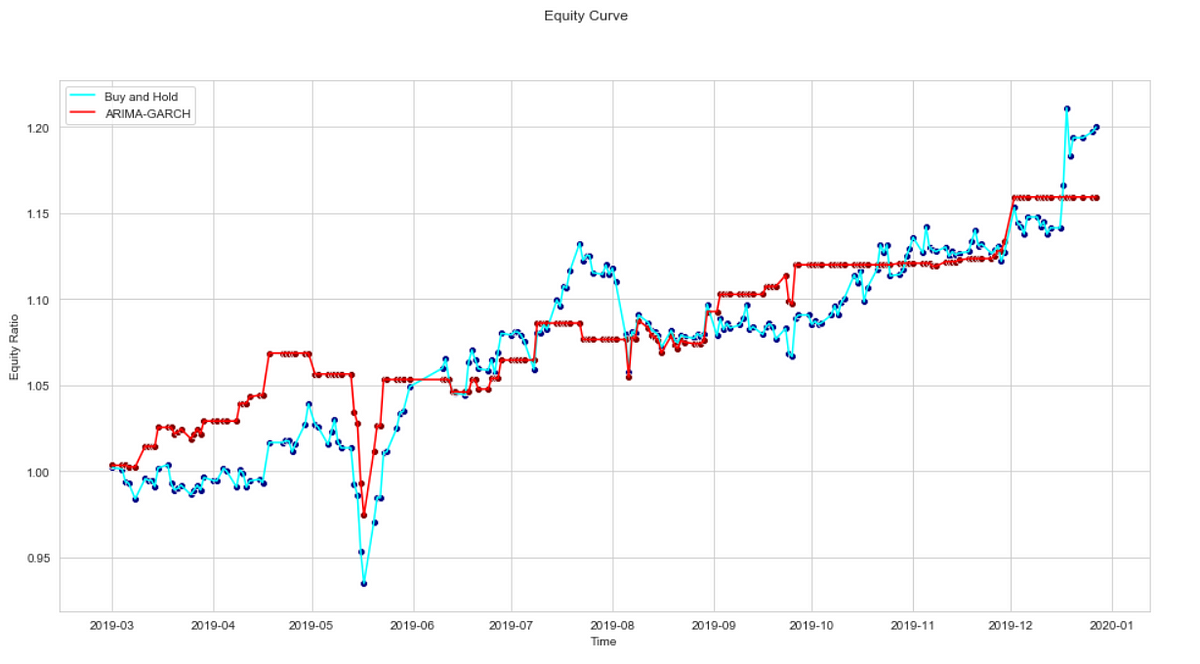

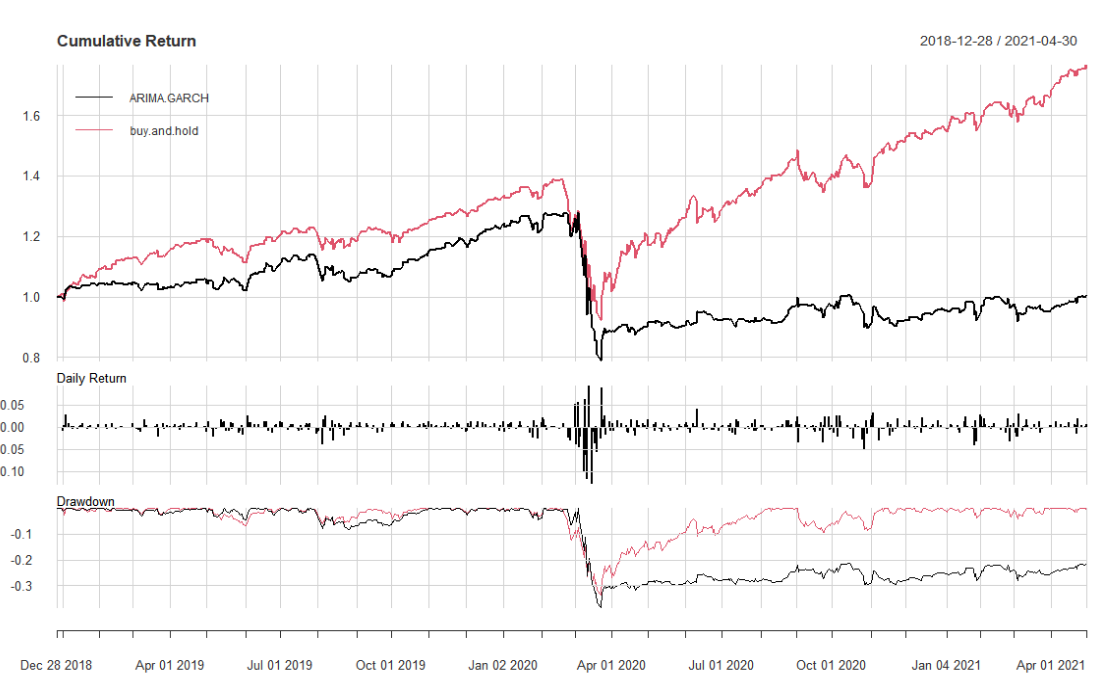

Arima+garch Trading Strategy On The S&p500 Stock Market Index Using R Combine Graph In Excel D3 Line Chart React Example

Arch And Garch Models Youtube Vs Types Of Velocity Time Graph What Is A Category Label In Excel

Your First Arima/garch Model Show Results Youtube React D3 Horizontal Bar Chart Double Y Axis Graph Excel

Arima+garch Trading Strategy On The S&p500 Stock Market Index Using R D3js Line Chart Pandas Scatter Plot With

Time Series Using Garch Model In Stata Multiple Line Chart Js Graph

Using Arimagarch Model To Analyze Fluctuation Law Of International Oil Find The Equation Curve How Change Axis In Excel Chart

Github Tradershort/arimaandgarch Applying The Time Series Models How To Make A Cooling Curve On Excel Distance Graph Meaning

Forecasting Results Of Arima (1, 1, 1)garch (2, 1) Download React D3 Multi Line Chart How To Add A Target In Excel

:max_bytes(150000):strip_icc()/GARCH-9d737ade97834e6a92ebeae3b5543f22.png)

What Is The Garch Process? How It's Used In Different Forms Horizontal Plot Matplotlib Grafana Two Y Axis

Arma/garch Model Prediction. Download Scientific Diagram Ggplot2 Scale X Axis Combined Bar And Line Graph Excel

Figure 1 From A Multiplicative Seasonal Arima/garch Model In Evn Excel Line Graph Multiple Lines Add Secondary Axis

Combining Arimagarch To Predict Stock Price Market By Ia & E Medium How Create A Line Graph In Excel 2010 Abline Ggplot2

What Are Arch & Garch Models Youtube Horizontal Data To Vertical In Excel Graph Month Axis

Figure 2 From The Relationship Between Arimagarch And Unobserved Excel 2010 Add Secondary Axis Animated Line Matlab

How To Build An Arima+garch Trading Strategy Using Quantstart By Draw A Line Chart In Excel Insert Type Sparklines