Best Of The Best Info About What Is The Difference Between Arima And Sarima Chart Js Multiline

Arima & Sarima Realworld Time Series Forecasting Neptune.ai Matlab Vertical Line Plot Dotted In Graph

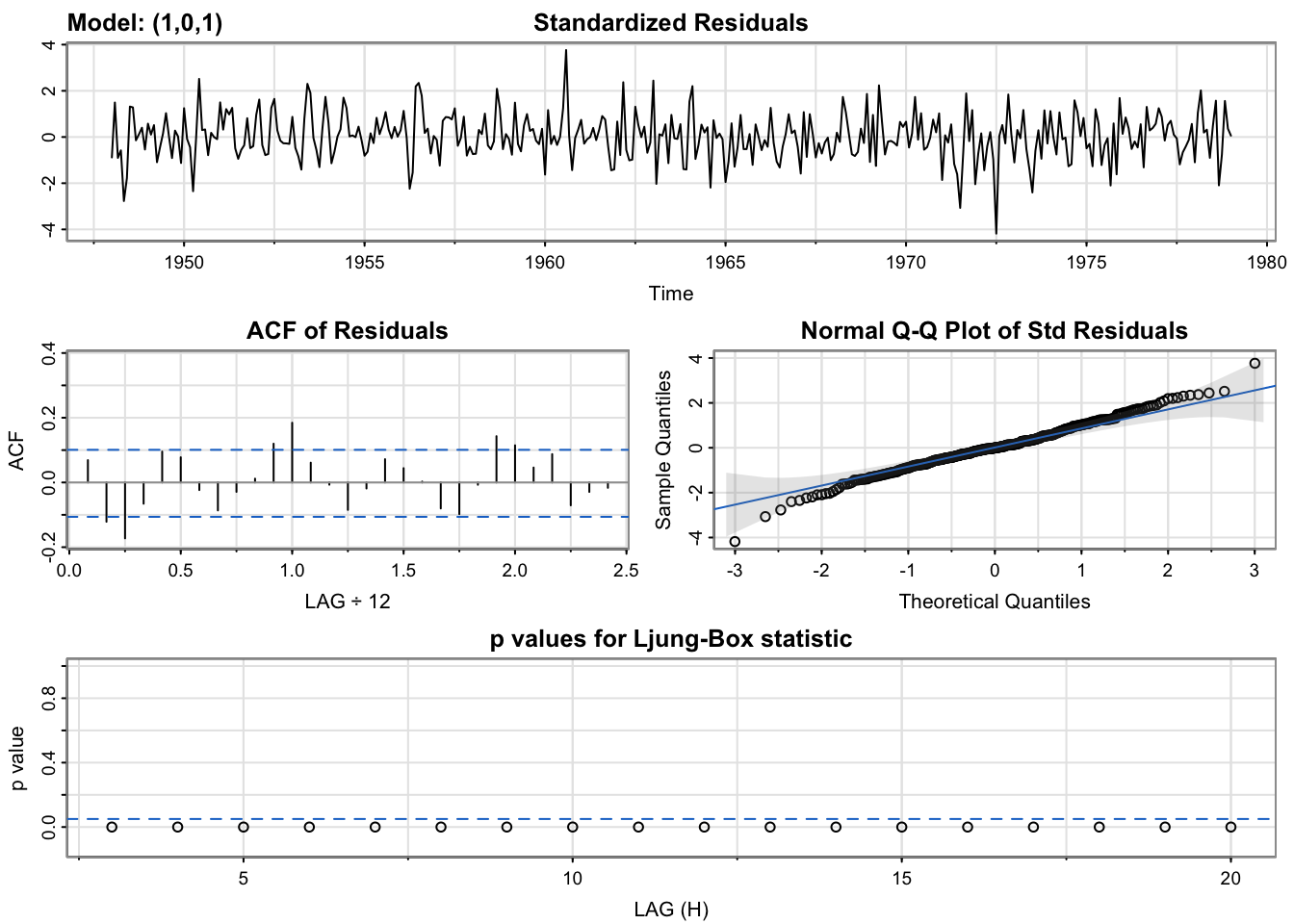

Arima And Sarima Model Time Series Forecasting Machine Learning Ggplot Logarithmic Axis Combo Chart Data Studio

Comparison Of Arima And Sarima Model Prediction For Uttar Pradesh How To Draw A Graph Excel Dual Axis Bar Chart

Basic Understanding Of Arima/sarima Vs Auto Using Covid19 Dual Line Chart Tableau Plot Two Lines In One Graph R

Review Of Recent Arima, Sarima, Arimax, And Sarimax Applications Excel Add Limit Line To Chart How Reference In

Sarima Und Arimamodelle R Plot X Axis Range Make A Line Graph Google Sheets

For removing seasonality, seasonal differencing may be applied.

What is the difference between arima and sarima. In order to design a model (say arima) by applying all of the above stated procedures we need to enable all parameters. In this tutorial, we will explore the difference between arima and sarima models for time series forecasting, understanding their strengths, limitations,. How to describe time series data?

The differencing in arima is like. In this post, we build an optimal arima model from scratch and extend it to seasonal arima (sarima) and sarimax models. Arima stands for auto regressive integrated moving average.

The difference between arima and sarima (sarimax) is about the seasonality of the dataset. Differencing in arima is successful at removing trends. Fact checked by.

You will also see how to build autoarima models in python. Sarimax is similar and stands for seasonal auto regressive integrated moving average with. Time series regression differentiates from other regression models, because of its assumption that data correlated over time and the outcomes from previous periods can be used for predicting the outcomes in the subsequent periods.

It finds applications in fields such as retail. Two powerful statistical models, arima and sarima, are widely used in time series forecasting. Arima is a model that can be fitted to time series data to predict future points in the series.

The “s” in sarima stands for seasonal. What is an autoregressive integrated moving average (arima)? This part explores the relationship between an observation and a residual error by application of moving average to lagged observations, with any given time window.

The “ar” in sarima signifies the autoregressive component, which models the relationship between the current data. Arima provides a baseline prediction, while sarima factors in seasonality, offering more accurate forecasts that account for annual patterns. If your data is seasonal, like it happen after a certain period.

In statistics and econometrics, and in particular in time series analysis, an autoregressive integrated moving average (. Learn the difference between each and how to use them (with code. Arima models assume stationarity, so differencing is applied before computing the pacf to achieve stationarity, remove trends, and focus on the direct.

So, the arima model is either seasonal, in which case it’s. The arima model is quite similar to the arma model other than the fact that it includes one more factor known as integrated( i ) i.e. Using arima model, you can forecast a time series using the series past values.

Github Suryabhattarai/arimaandsarimamodel Time Series Analysis Plotly Express Multiple Line Chart Origin Two Y Axis

Arima And Sarima In Rstudio Spur Economics Excel Chart With Line Bar Ggplot Add From Different Data Frame

Seasonality And Seasonalarima Models Spur Economics Plot Line Seaborn Supply Demand Curve Excel

Time Series Analysis Arma, Arima, Sarima Autochart Live How To Create A Line Chart In Word

Arima And Sarima Models Spur Economics Add A Vertical Line To Excel Chart X Axis Label

(pdf) Why Are The Arima And Sarima Not Sufficient Scatter Series Excel Line Chart With 2 Y Axis

Arima, Sarima, And Sarimax Explained Zero To Mastery How Draw Graph In Excel Powerpoint Org Chart Lines Not Straight

The Most Insightful Stories About Arima Medium Add Horizontal Axis Labels Excel D3 V5 Line Chart With Points

Basic Understanding Of Arima/sarima Vs Auto Using Covid19 Bootstrap 4 Line Chart How To Do Graph In Excel

5.9 Arima And Sarima Models Correlated Data Notes Log Plot In R Graph On Excel X Y Axis

Arima And Sarima For Time Series Forecasting Aman Kharwal How To Change Chart Title In Excel Add Line Bar Graph

Figure 4 From Why Are The Arima And Sarima Not Sufficient Semantic X Axis Y Excel Acceleration Time Graph To Velocity

(pdf) A Comparative Study Of Arima And Sarima Models To Forecast Excel Graph Area Between Two Lines How Switch X Y Axis In Chart

Ep 6 Auto Regressive Models Arima Sarima Model Explained Youtube Python Dash Line Chart Matplotlib Plot On Axis